[Source: Gaogong LED's "LED Research Review" February issue / GLII Yu Bin] According to the latest report released by the High-tech LED Industry Research Institute (GLII), the output value of LED chips in mainland China in 2012 (including Taiwanese capital, foreign investment) The output value of the production base in mainland China, the same as the next) 7.2 billion yuan. Affected by the sharp drop in chip prices last year, the output value only achieved a 20% increase in the case of a year-on-year increase in output of nearly 80%. Among them, the growth of chip output value mainly depends on the output value of Taiwanese-funded enterprises and foreign-funded enterprises in the mainland, and the growth of output value of local chip companies is not obvious.

Local enterprises' output growth is only 6%

In 2012, mainland China's local LED chip companies achieved an output value of only 5.1 billion yuan, a year-on-year increase of only 6%. Among them, the output value of a number of chip companies decreased year-on-year.

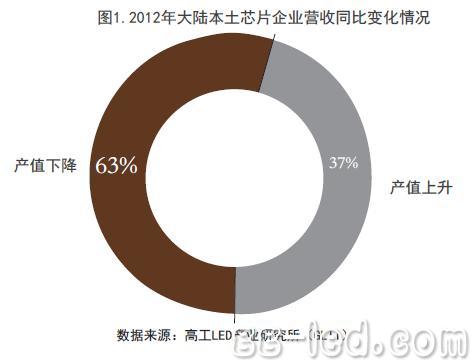

Excluding the number of new production or exiting enterprises, the number of enterprises with an increase in output value in 2012 was 13 (37%); the number of enterprises with a year-on-year decline in output value was 22, accounting for 63%.

The decline in the output value of most chip companies is mainly affected by the rapid decline in product prices. According to GLII data, in 2012, the price of LED chips in mainland China continued to decline sharply in 2011. The average price dropped by 32% year-on-year, and some products fell by as much as 50%.

Two levels of differentiation in the industry gradually emerged

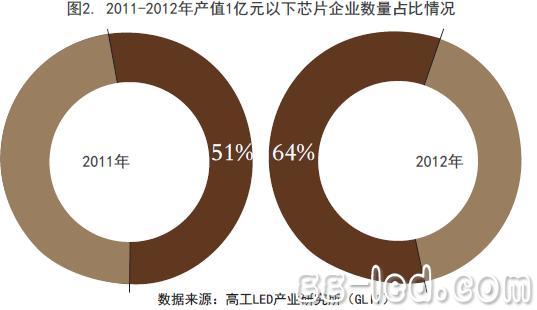

In 2011, the number of domestically produced chips in mainland China was 35, of which 18 were under 100 million yuan, accounting for 51%. By 2012, the number of production enterprises was 36, and the number of enterprises with an output value of less than 100 million yuan was 23, accounting for 64%.

The total output value of the top five chip companies in 2012 accounted for 55% of the total output value of the industry, an increase of 4.2 percentage points over 2011. Among them, the average output value of enterprises with an output value of more than 100 million yuan was 315 million yuan, an increase of 27% over 2011. GLII believes that the polarization trend of LED upstream chip industry is gradually emerging, the industry has entered the survival of the fittest period ahead of schedule, and industry consolidation has accelerated.

Industry integration has started

In 2012, the merger and acquisition of two LED chip companies in mainland China announced that the LED upstream chip industry integration war has started.

On November 13, 2012, Sanan Optoelectronics announced that it plans to use self-raised funds of no more than 2.352 billion Taiwan dollars (about 506 million yuan) to subscribe for no more than 120 million ordinary shares issued by Yanyuan Optoelectronics in private placement. Upon completion of the transaction, Sanan Optoelectronics will hold approximately 19.9% ​​of the shares of Yanyuan Optoelectronics and become the largest shareholder of Yanyuan Optoelectronics. On February 19, 2013, the relevant departments of Taiwan, China confirmed that they had received the investment in the investment of Sanan Optoelectronics.

On December 27, 2012, Dehao Runda issued the “Significant Equity Acquisition Announcementâ€, and the wholly-owned subsidiary Hong Kong Dehao Runda purchased 8.24% of NVC Lighting, and passed NVC Inc., one of the major shareholders of NVC Lighting. Signing the “Share Transfer Agreement†with the conditions for entry into force, and accepting 11.81% of the shares of NVC held by it. If the "Share Transfer Agreement" is fulfilled, Dehao Runda will eventually account for 20.5% of NVC and become the largest shareholder.

In 2012, due to the lower-than-expected demand in the downstream application market and the rapid expansion of upstream capacity, the price war on LED chips has intensified. The continued decline in chip prices has led to a decline in corporate profitability, and most chip companies are already on the verge of losing money. The cruel market situation has led some chip companies to choose to be forced to withdraw. In addition, projects that have not yet been put into production are making slow progress and do not rule out the possibility of exiting at any time.

GLII believes that the LED upstream chip industry has gradually shifted from the original technology competition to scale and capital competition. Many SMEs have caused some capacity to be released due to the capital chain bottleneck.

A chip company official told GLII that the company's newly developed LED display chip is very cost-effective, and customer feedback is also very good, but due to funding shortages and price competition, the company had to give up this new product.

For small and medium-sized enterprises, most of them do not have the advantages of scale and strong financial support, and the follow-up enterprise development will be difficult.

In the market environment of “going against the water, not going back,†integration or integration may be a way out. GLII expects that 2013 will be the transition year for the upstream chip industry integration. Industrial integration will be carried out on a large scale in 2014.

Challenges and opportunities in 2013

In 2013, it will still be a tough year for mainland Chinese chip companies. Overcapacity is still difficult to alleviate in the short term.

As of the end of 2012, the number of domestic MOCVD has reached 917, and last year's MOCVD capacity utilization rate was only about 30%. It is expected that the overall capacity utilization rate will still be more than 60% this year.

Overcapacity will inevitably lead to price wars continuing to ferment, and corporate profitability will still be difficult to improve. 2013 will be a challenging year, but it is also a year full of opportunities.

After several years of technology precipitation, the overall performance of local chip products in mainland China has been greatly improved, and some products have been widely used in low-end indoor lighting products.

GLII expects that the LED lighting chip market will grow by more than 60% in 2013. As the market share of mainland domestic chips continues to increase, the overall growth rate will be greater than the market demand growth rate. For companies that have the ability to seize opportunities, 2013 will be a year of hope.

Local enterprises' output growth is only 6%

In 2012, mainland China's local LED chip companies achieved an output value of only 5.1 billion yuan, a year-on-year increase of only 6%. Among them, the output value of a number of chip companies decreased year-on-year.

Excluding the number of new production or exiting enterprises, the number of enterprises with an increase in output value in 2012 was 13 (37%); the number of enterprises with a year-on-year decline in output value was 22, accounting for 63%.

The decline in the output value of most chip companies is mainly affected by the rapid decline in product prices. According to GLII data, in 2012, the price of LED chips in mainland China continued to decline sharply in 2011. The average price dropped by 32% year-on-year, and some products fell by as much as 50%.

Two levels of differentiation in the industry gradually emerged

In 2011, the number of domestically produced chips in mainland China was 35, of which 18 were under 100 million yuan, accounting for 51%. By 2012, the number of production enterprises was 36, and the number of enterprises with an output value of less than 100 million yuan was 23, accounting for 64%.

The total output value of the top five chip companies in 2012 accounted for 55% of the total output value of the industry, an increase of 4.2 percentage points over 2011. Among them, the average output value of enterprises with an output value of more than 100 million yuan was 315 million yuan, an increase of 27% over 2011. GLII believes that the polarization trend of LED upstream chip industry is gradually emerging, the industry has entered the survival of the fittest period ahead of schedule, and industry consolidation has accelerated.

Table 1. The output value of the top five enterprises in 2011-2012 and the average output value of enterprises in 100 million yuan

Industry integration has started

In 2012, the merger and acquisition of two LED chip companies in mainland China announced that the LED upstream chip industry integration war has started.

On November 13, 2012, Sanan Optoelectronics announced that it plans to use self-raised funds of no more than 2.352 billion Taiwan dollars (about 506 million yuan) to subscribe for no more than 120 million ordinary shares issued by Yanyuan Optoelectronics in private placement. Upon completion of the transaction, Sanan Optoelectronics will hold approximately 19.9% ​​of the shares of Yanyuan Optoelectronics and become the largest shareholder of Yanyuan Optoelectronics. On February 19, 2013, the relevant departments of Taiwan, China confirmed that they had received the investment in the investment of Sanan Optoelectronics.

On December 27, 2012, Dehao Runda issued the “Significant Equity Acquisition Announcementâ€, and the wholly-owned subsidiary Hong Kong Dehao Runda purchased 8.24% of NVC Lighting, and passed NVC Inc., one of the major shareholders of NVC Lighting. Signing the “Share Transfer Agreement†with the conditions for entry into force, and accepting 11.81% of the shares of NVC held by it. If the "Share Transfer Agreement" is fulfilled, Dehao Runda will eventually account for 20.5% of NVC and become the largest shareholder.

In 2012, due to the lower-than-expected demand in the downstream application market and the rapid expansion of upstream capacity, the price war on LED chips has intensified. The continued decline in chip prices has led to a decline in corporate profitability, and most chip companies are already on the verge of losing money. The cruel market situation has led some chip companies to choose to be forced to withdraw. In addition, projects that have not yet been put into production are making slow progress and do not rule out the possibility of exiting at any time.

GLII believes that the LED upstream chip industry has gradually shifted from the original technology competition to scale and capital competition. Many SMEs have caused some capacity to be released due to the capital chain bottleneck.

A chip company official told GLII that the company's newly developed LED display chip is very cost-effective, and customer feedback is also very good, but due to funding shortages and price competition, the company had to give up this new product.

For small and medium-sized enterprises, most of them do not have the advantages of scale and strong financial support, and the follow-up enterprise development will be difficult.

In the market environment of “going against the water, not going back,†integration or integration may be a way out. GLII expects that 2013 will be the transition year for the upstream chip industry integration. Industrial integration will be carried out on a large scale in 2014.

Challenges and opportunities in 2013

In 2013, it will still be a tough year for mainland Chinese chip companies. Overcapacity is still difficult to alleviate in the short term.

As of the end of 2012, the number of domestic MOCVD has reached 917, and last year's MOCVD capacity utilization rate was only about 30%. It is expected that the overall capacity utilization rate will still be more than 60% this year.

Overcapacity will inevitably lead to price wars continuing to ferment, and corporate profitability will still be difficult to improve. 2013 will be a challenging year, but it is also a year full of opportunities.

After several years of technology precipitation, the overall performance of local chip products in mainland China has been greatly improved, and some products have been widely used in low-end indoor lighting products.

GLII expects that the LED lighting chip market will grow by more than 60% in 2013. As the market share of mainland domestic chips continues to increase, the overall growth rate will be greater than the market demand growth rate. For companies that have the ability to seize opportunities, 2013 will be a year of hope.

Touch Panel For Iphone,Touch Screen Digitizer Panel,Touch Screen Panel For Iphone,Phone Touch Screen

Shenzhen Xiangying touch photoelectric co., ltd. , https://www.starstp.com